Onward!!

But the first half may be hard to duplicate

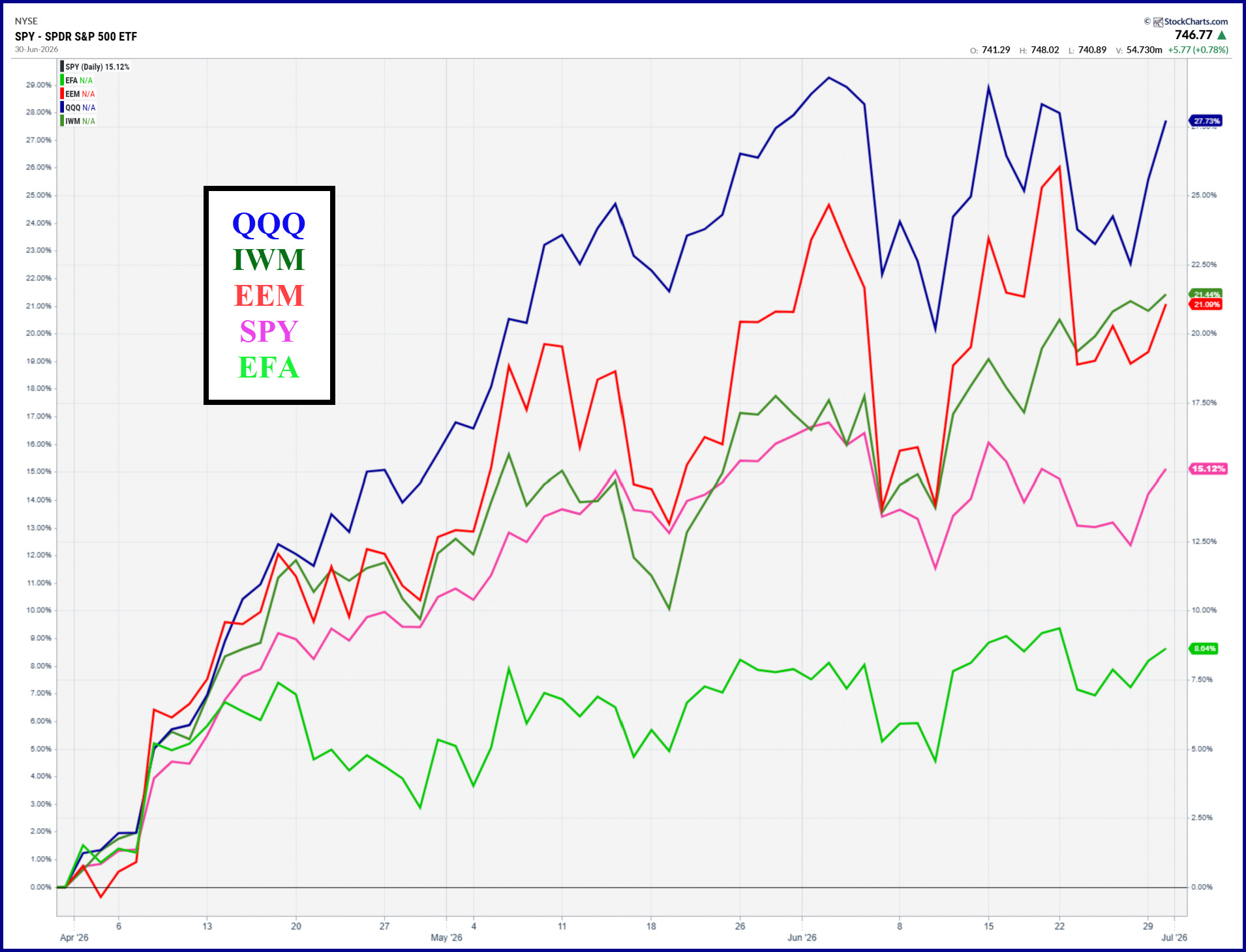

Q2 and the first half of 2026 are in the books and you wanted to own equities. The first chart below is year-to-date performance for the S&P 500 (SPY), Nasdaq 100 (QQQ), Russell 2000 small caps (IWM), developed international (EFA) and emerging markets (EEM). Emerging markets were the winner from the start of the year.

Looking at only the second quarter, the W goes to the triple Qs and small caps nudged out emerging markets. SPY came in fourth and developed international lagged the group. If you’re wondering how emerging markets have done so well, look no further than the list of EEM holdings dominated by Taiwan Semi, Samsung and SK Hynix. Call them the Mag 3.

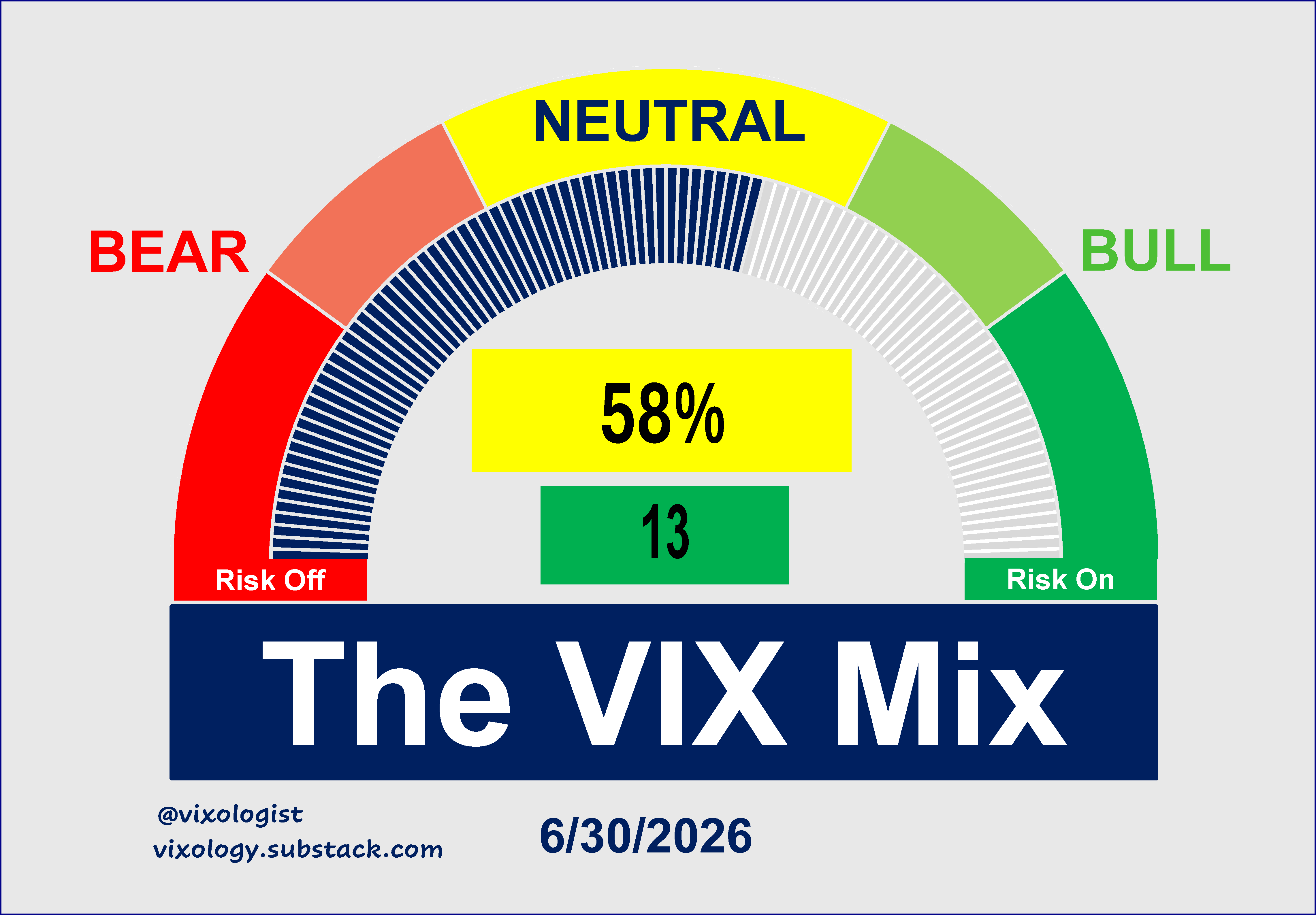

Back in the US volatility complex, we finished the first half with the VIX Mix in the upper half of the Neutral slice having picked up 13 points on the last day of the quarter. We also saw a distinct positive flip among the 17 components with a pickup of six bullish (seven in total) and only one still on the bullish side (that rascal VIX-VOLI spread).

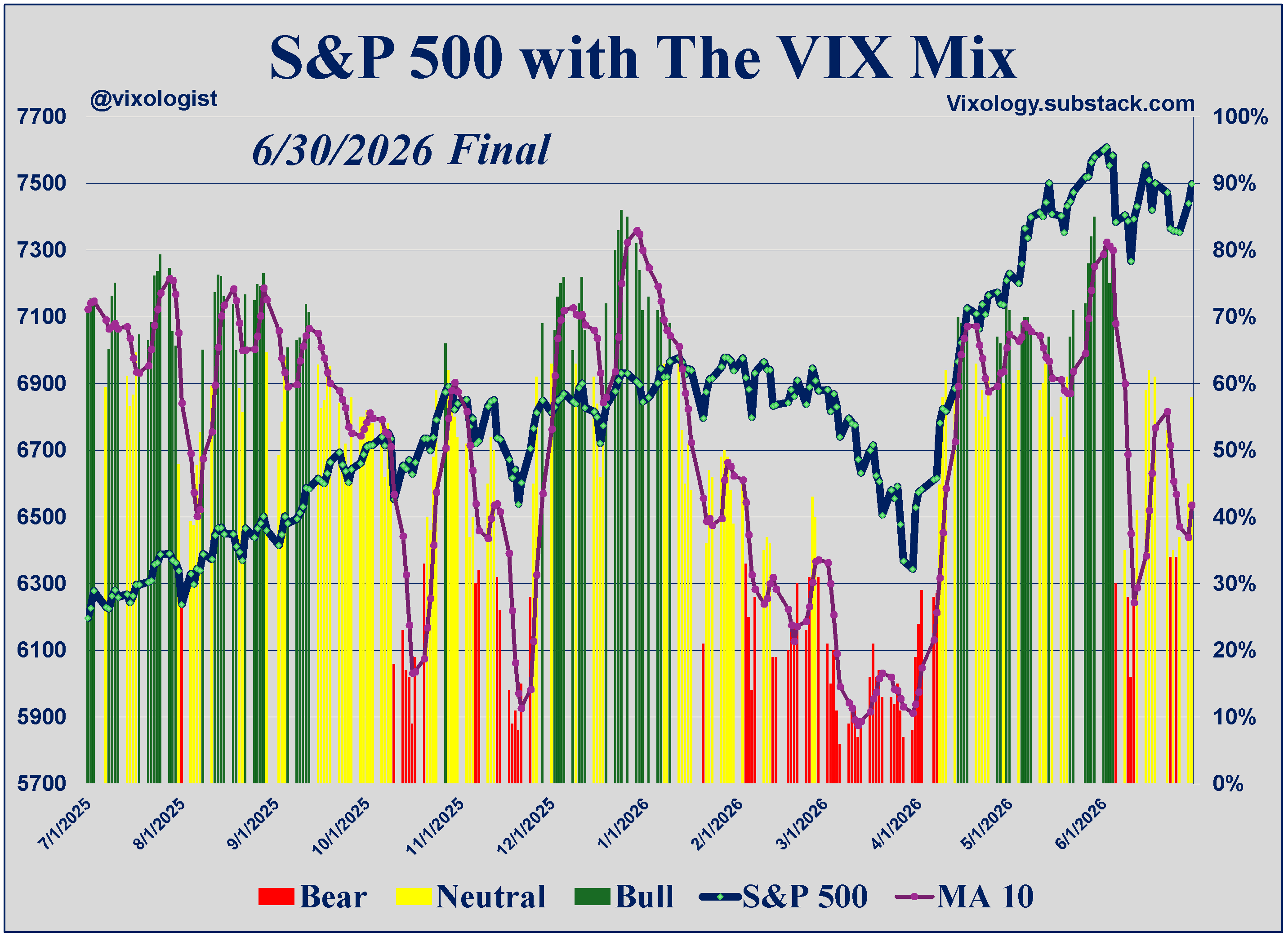

Yesterday’s positive move was enough to turn our 10-day trend line back to the north, giving chase to this week’s recovery for SPX.

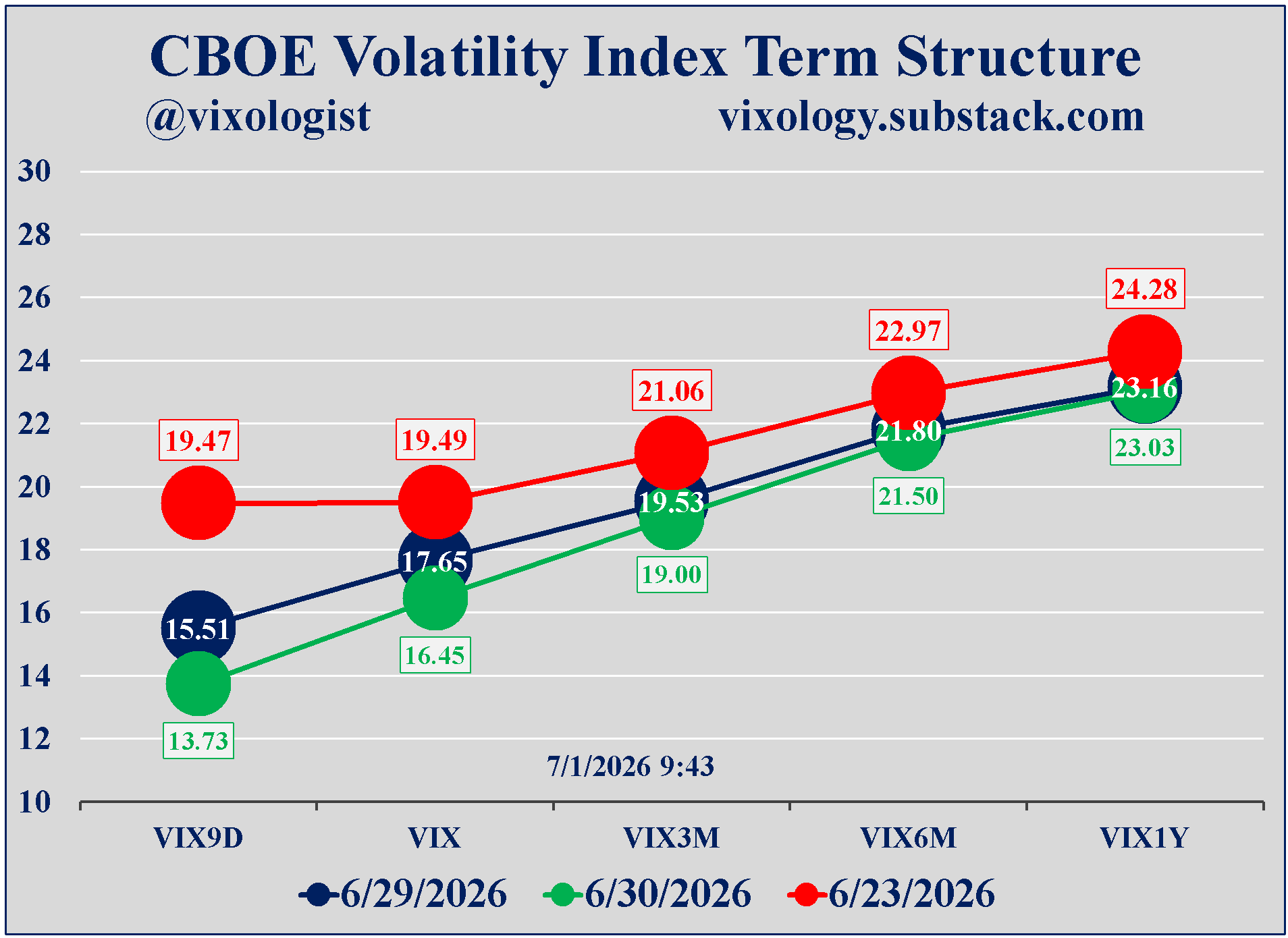

Yesterday we noted the improvement in the CBOE volatility term structure after last week’s “scare” and we have further improvement as shown below. Investors are pretty comfortable that nothing scary is on the horizon.

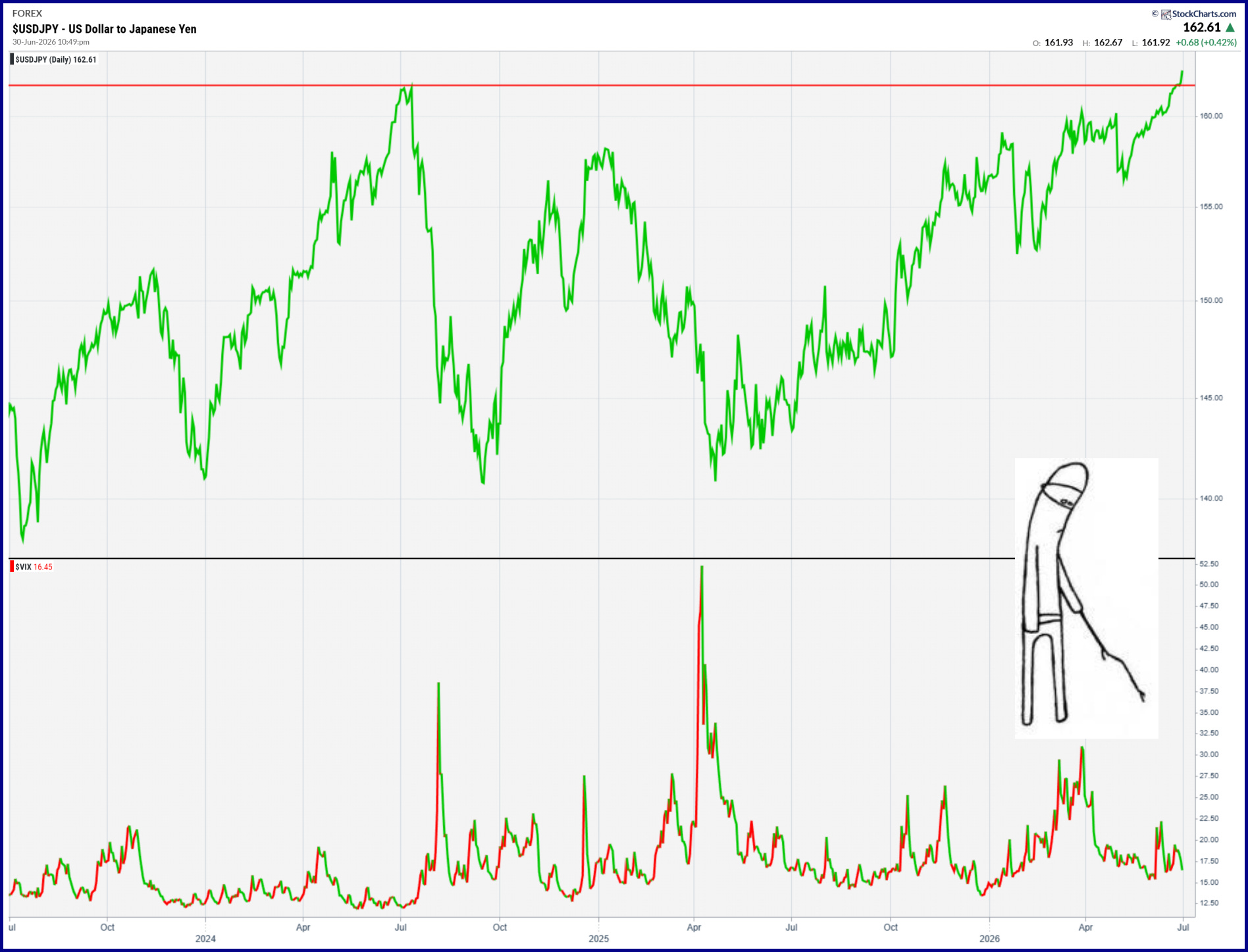

And yet, the internet is buzzing with concerns about what Japan may do to address significant weakness in the Yen. The USD/JPY cross has poked above a level that has previously seen intervention by the Bank of Japan and everyone should remember the contribution to equity market volatility that came in late July of 2024. The only reason to not be concerned is that everyone seems to be watching this and that may be why VIX appears to be ignoring the breakout. But one possibility is that the BOJ does something on Friday while US markets are closed for the 4th of July. That might lead to some turmoil come next Monday. You can’t be surprised.

All content presented here is for informational and educational purposes only. Distribution of any content to any persons other than the recipient is unauthorized. Furthermore, any alteration of content presented here is prohibited. By accepting delivery of this presentation, the reader agrees to the foregoing. Certain information presented herein has been obtained from third-party sources considered to be reliable, but there is no guarantee of completeness or accuracy and it should not be relied upon as such. There is no obligation to update or correct any information presented. Readers should not treat any statement, opinion or viewpoint expressed herein as a solicitation or recommendation to buy or sell any security or follow any investment strategy. This material does not consider the investment objectives, financial situation, or needs of any particular reader. Readers should seek advice from a qualified financial or investment advisor prior to making any investment decision.