Almost Halftime

Are the winds shifting?

Today’s close will bring us to the end of June and the halfway point of 2026. Watch for our Vixology Halftime Report coming your way.

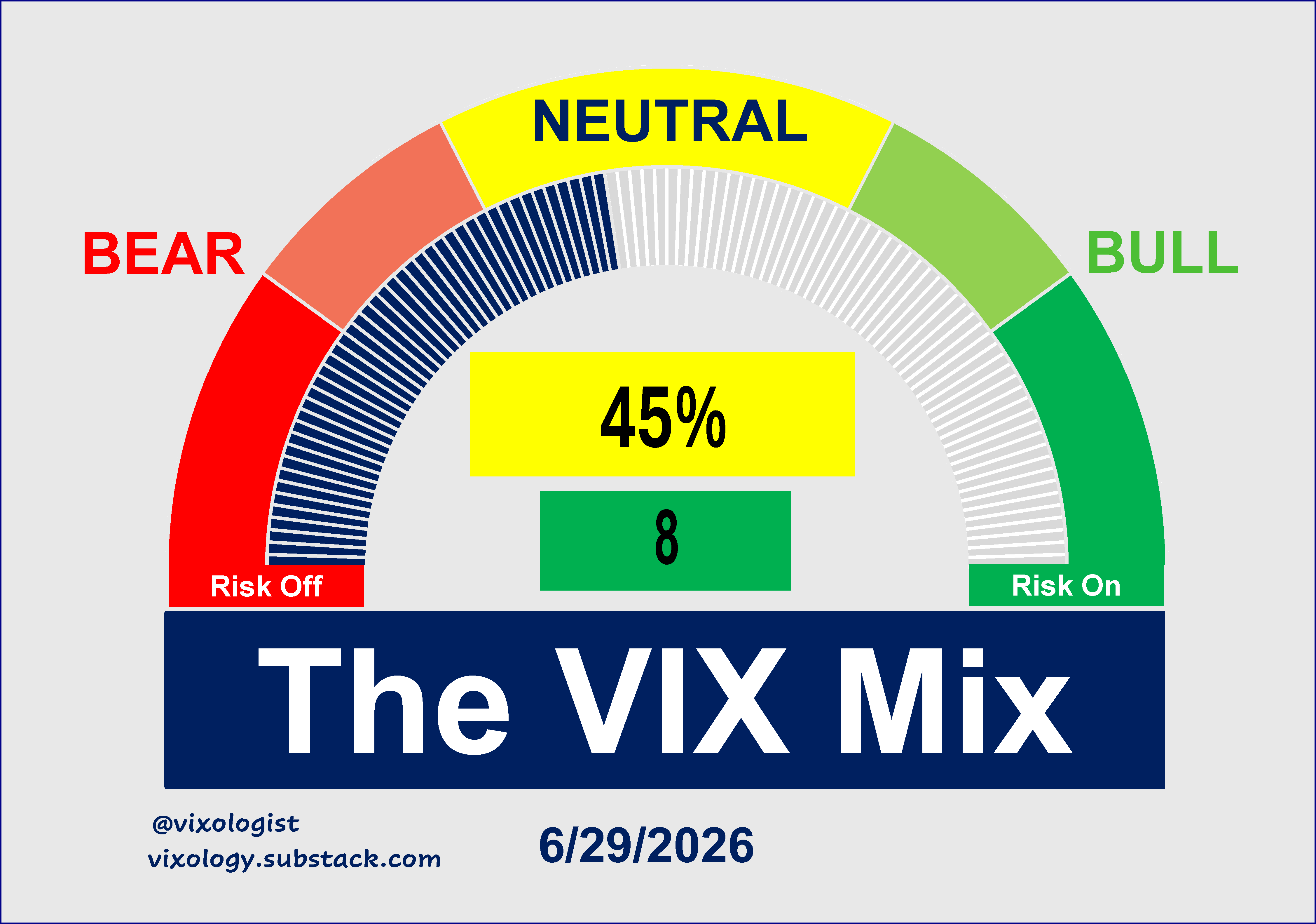

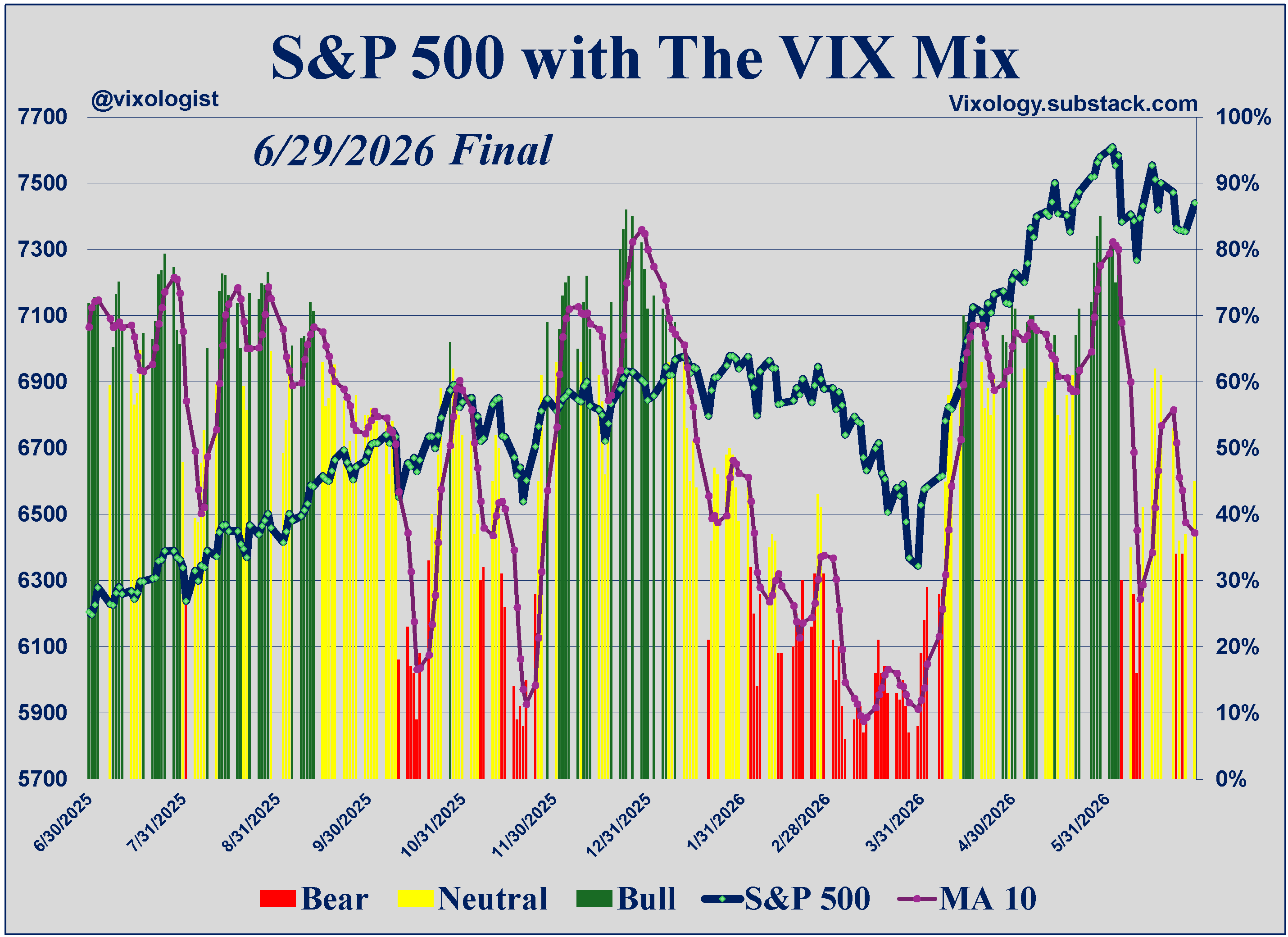

Judging by the recent performance of the VIX Mix, June should end on a relatively positive note. Not great, but better. Yesterday’s reading came in at 45% with an eight-point pickup. We also saw one component turn green while the bearish count dropped from nine to two.

As seen below, the trend line for the Mix continues to point down (not good) but should be less bad if we get another positive day for equity markets to close Q2.

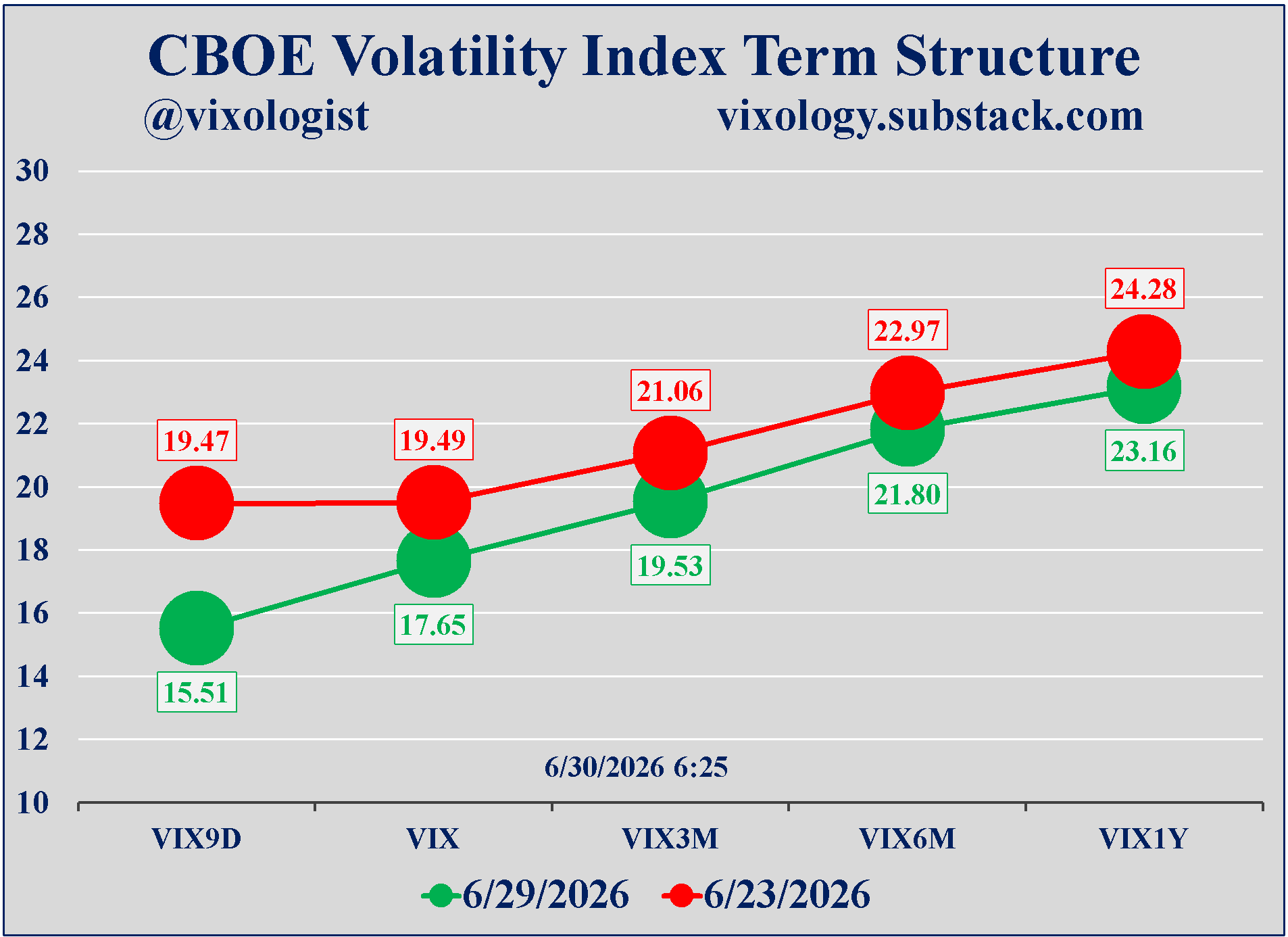

The component that turned bullish yesterday is one that looks to the CBOE volatility term structure. You can see below that two things have change over the past week. First, each of the five data points we care about were lower. And the VIX 9-Day showed the biggest drop as investors relaxed about the potential for something bad to happen in the very near term.

A couple more charts reflecting on what appears to be a shift by investors to pare back on Mag 7/large cap growth and add to everything else. The first chart compares the cap-weighted SPY to its equal-weight brother (RSP). Going back to the Tariff Tantrum bottom, SPY has outperformed RSP but the latter has picked up some relative strength in June.

Next, we look at how small cap stocks have fared over the same time period. Even with the to-be-expected wiggles in the relative strength line, the Russell 2000 small caps (IWM) have created some separation from their large cap cousin.

The strength of both RSP and IWM are signs that US equity markets may continue to carry on higher even if we see weakness in the handful of mega-caps that have been driving performance. We suspect that this market dynamic will be the big story for the second half of the year. Having said that, we will be keeping a close eye on credit markets. Bad news from that corner could create a headwind for equities of all sizes.

All content presented here is for informational and educational purposes only. Distribution of any content to any persons other than the recipient is unauthorized. Furthermore, any alteration of content presented here is prohibited. By accepting delivery of this presentation, the reader agrees to the foregoing. Certain information presented herein has been obtained from third-party sources considered to be reliable, but there is no guarantee of completeness or accuracy and it should not be relied upon as such. There is no obligation to update or correct any information presented. Readers should not treat any statement, opinion or viewpoint expressed herein as a solicitation or recommendation to buy or sell any security or follow any investment strategy. This material does not consider the investment objectives, financial situation, or needs of any particular reader. Readers should seek advice from a qualified financial or investment advisor prior to making any investment decision.

Gex positioning for july Opex is considerebly bearish, so after hunky-dory 4th of July celebration I will probably go “back on the chain gang”